After a brief recovery to $41,000 on June 14, Bitcoin (BTC) investors might have thought that the bear market was finally over. After all, it was the highest level since May 21 and the date that MicroStrategy (MSTR) announced a successful $500 million debt offering.

The funds are usually available in one or two business days, and the proceeds would be used to acquire even more Bitcoin for the business intelligence company’s balance sheet. MicroStrategy followed this fund-raise with another surprise filing to sell up to $1 billion of its stock to buy even more Bitcoin.

However, a 30% drop took place over the following week, causing Bitcoin to reach its lowest level since January 22. The $28,800 bottom might have lasted less than fifteen minutes, but the bear sentiment was already established.

The sell-off was largely attributed to Chinese miners’ capitulating after they were forced to abruptly shut down their operations. Furthermore, on June 21, an official People’s Bank of China (PBoC) reiterated that all banks and payment institutions “must not provide account opening or registration for [virtual currency]-related activities.”

The open question is whether derivatives played a vital part in the correction or at least displayed stress signs that may indicate an even more dangerous second leg down?

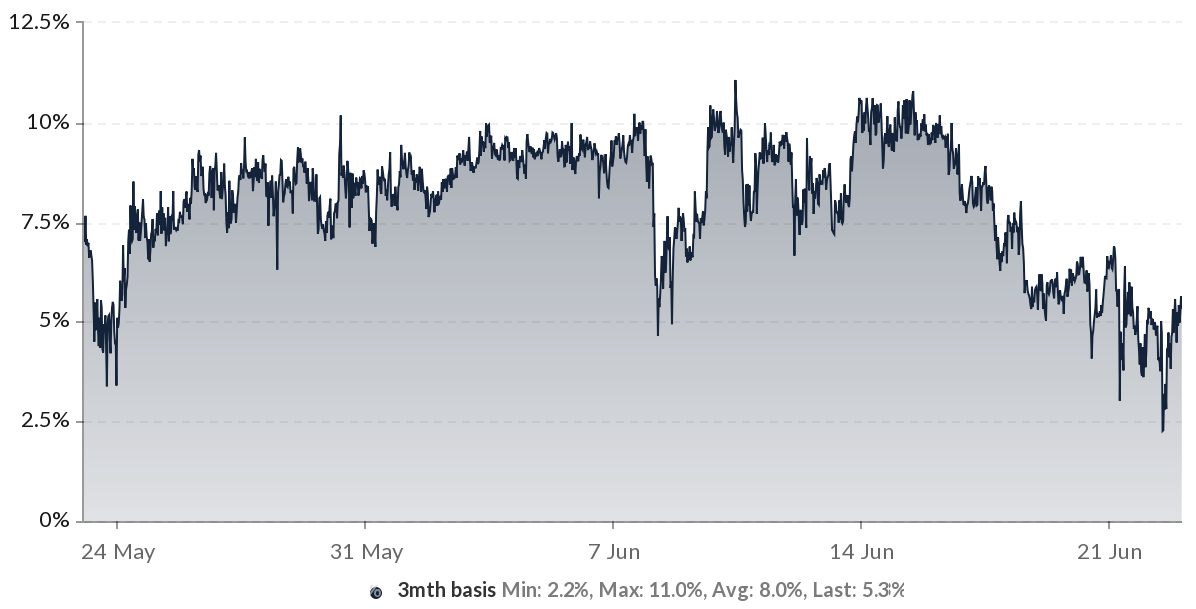

The futures premium showed no signs of backwardation

The futures premium (or basis) measures the gap of longer-term futures contracts to the current spot (regular markets) levels. Whenever this indicator fades or turns negative, this is an alarming red flag. This situation is also known as backwardation and indicates a bearish sentiment.

Huobi 3-month Bitcoin futures basis. Source: Skew

Huobi 3-month Bitcoin futures basis. Source: Skew

Futures should trade at a 5% to 15% annualized premium in healthy markets, otherwise known as contango. On the worst moment on June 22, this basis bottomed at 2.5%, which is considered bearish but not enough to trigger any red flag.

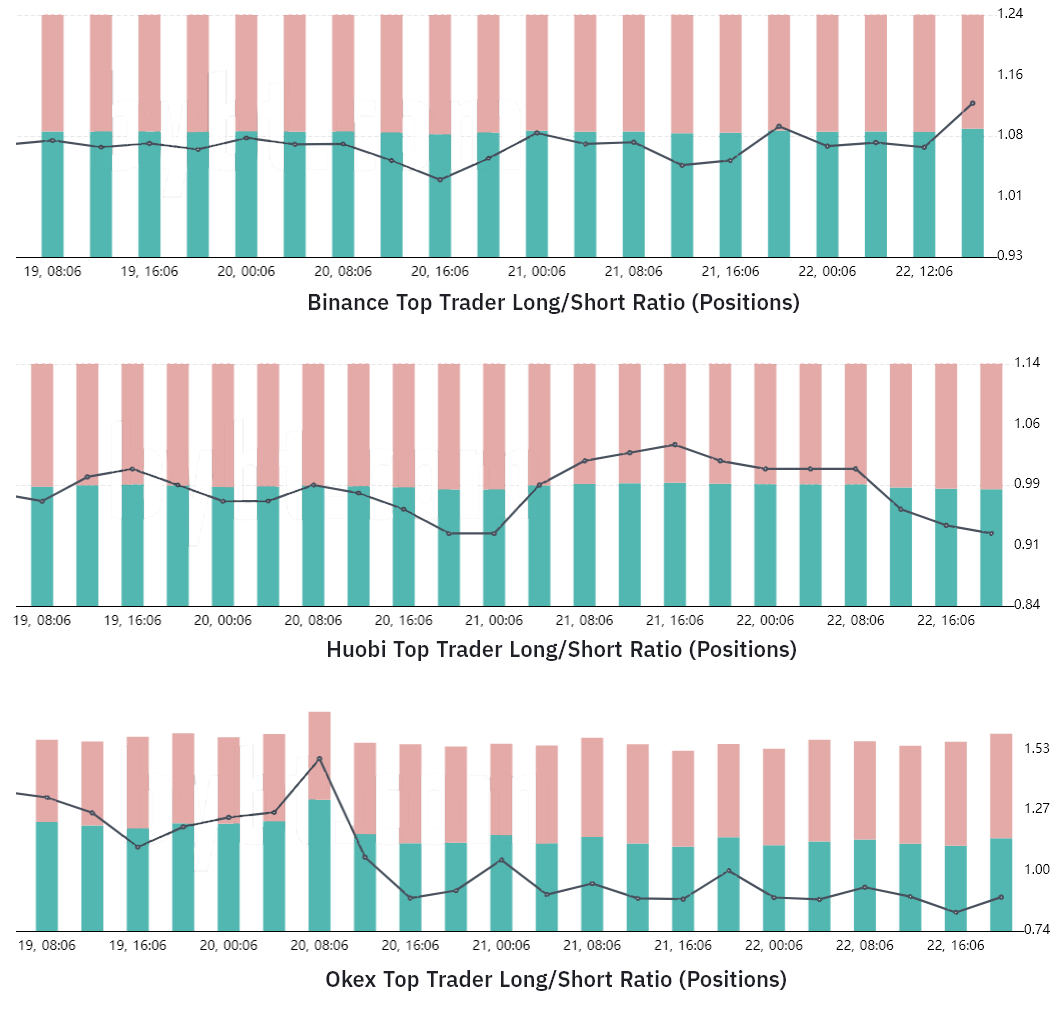

There was zero panic from top traders

The top traders’ long-to-short indicator is calculated using clients’ consolidated positions, including spot, margin, perpetual and futures contracts. This metric gathers a broader view of professional traders’ effective net position.

Derivatives exchanges’ top traders long-to-short ratio. Source: Bybt

Derivatives exchanges’ top traders long-to-short ratio. Source: Bybt

Despite the discrepancies between crypto exchange methodologies, analyzing changes over time provides valuable insights. Top traders at Binance, for example, increased their long positions relative to shorts on June 22.

At Huobi, there has been some increase in their net short exposure, but nothing out of the ordinary as the indicator reached the same level two days before.

Lastly, OKEx top traders reduced their longs on June 20 and have since kept a 0.80 level favoring shorts by 20%.

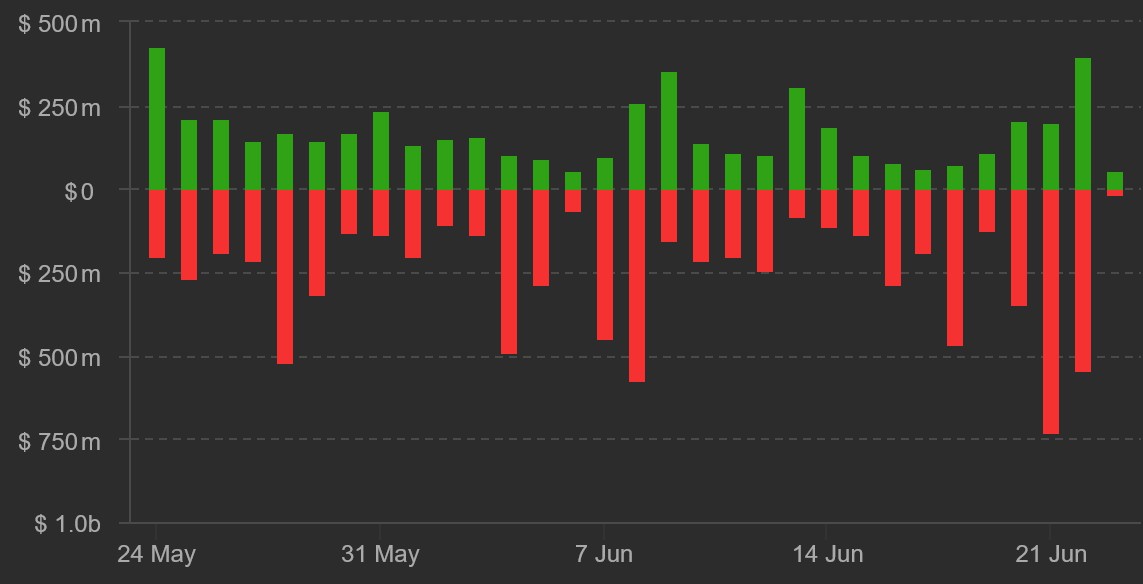

Long futures liquidations were less than $600 million

Those unaware of the price swing would never have guessed that Bitcoin traded below $29,000 based on futures liquidations data.

Aggregate futures liquidations (longs in red). Source. Coinalyze.net

Aggregate futures liquidations (longs in red). Source. Coinalyze.net

Less than $600 million in longs were liquidated on June 22, lower than the previous day’s $750 million figure. Had longs been overleveraged, a 20% drop in less than two days would have triggered stop orders of a much greater size.

Data show no current signs of stress from longs or a potential negative swing caused by derivatives markets.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.