“Don’t fight the trend” is an old saying in the markets, and there are other variants of the phrase like “never catch a falling knife.” The bottom line is that traders should not try to anticipate trend reversals, or even worse, try to improve their average price while losing money.

It really doesn’t matter whether one is trading soy futures, silver, stocks or cryptocurrencies. Markets generally move in cycles, which can last from a few days to a couple of years. In Bitcoin’s (BTC) case, it’s hard for anyone to justify a bullish case by looking at the chart below.

Bitcoin price in USD at Coinbase. Source: TradingView

Bitcoin price in USD at Coinbase. Source: TradingView

Over the past 25 days, every attempt to break the descending channel has been abruptly interrupted. Curiously, the trend points to sub-$40,000 by mid-October, which happens to be the deadline for the United States Securities and Exchange Commission decision on the ProShares Bitcoin ETF (Oct. 18) and Invesco Bitcoin ETF (Oct. 19).

According to the CoinShares weekly report, the recent price action triggered institutional investors to enter the sixth consecutive week of inflows. There has been nearly $100 million worth of inflows between Sept. 20 and 24.

Experienced traders claim that Bitcoin needs to reclaim the $43,600 support for the bullish trend to resume. Meanwhile, on-chain data points to heavy accumulation, as the falling exchange supply has been dominant.

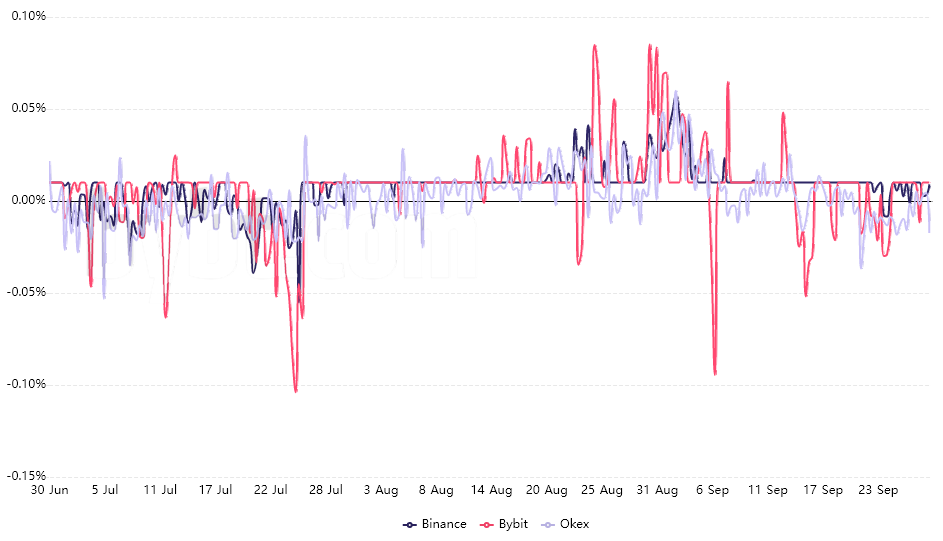

Perpetual futures show traders neutral to bearish

To gauge investor sentiment, one should analyze the funding rate on perpetual contracts because these are retail traders’ preferred instruments. Unlike monthly contracts, perpetual futures (inverse swaps) trade at a very similar price to regular spot exchanges.

The funding rate is automatically charged every eight hours from longs (buyers) when demanding more leverage. However, when the situation is reversed, and shorts (sellers) are over-leveraged, the funding rate turns negative, and they become the ones paying the fee.

Bitcoin perpetual futures 8-hour funding rate. Source: Bybt.com

Bitcoin perpetual futures 8-hour funding rate. Source: Bybt.com

A ‘neutral’ situation involves leverage longs paying a small fee, oscillating from 0% to 0.03% per eight-hour period, which is equivalent to 0.6% per week. Yet, the above chart shows a slightly bearish trend since Sept. 13, when the funding rate was last seen above the 0.03% threshold.

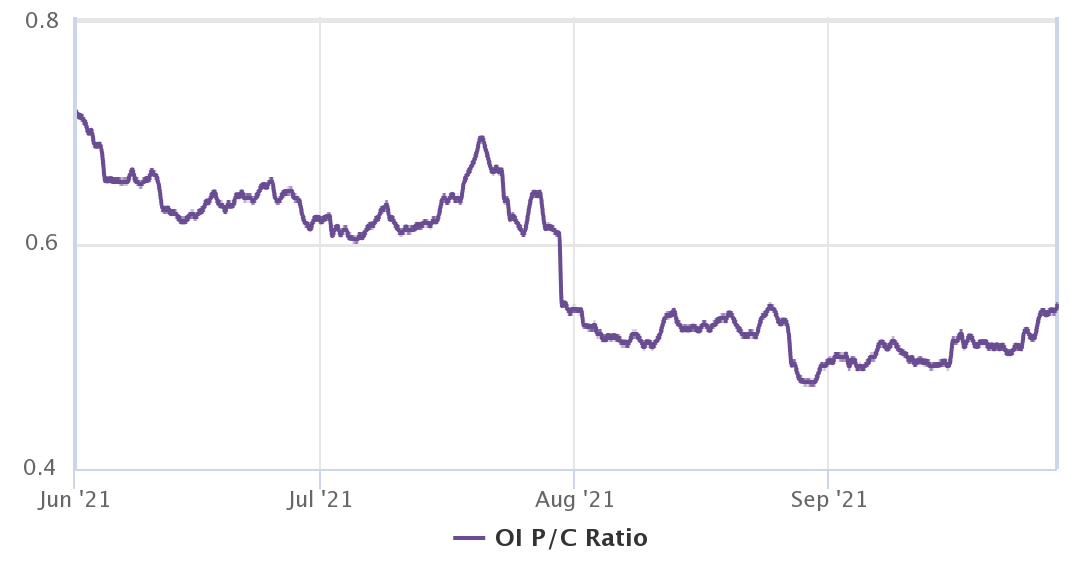

The put-to-call ratio favors bulls, but the trend has changed

Unlike futures contracts, options are divided into two segments. Call (buy) options allow the buyer to acquire Bitcoin at a fixed price on the expiry date. Generally speaking, these are used on either neutral arbitrage trades or bullish strategies.

Meanwhile, the put (sell) options are commonly used as protection from negative price swings.

To understand how these competing forces are balanced, one should compare the calls and put options open interest.

Bitcoin options open interest put-to-call ratio. Source: Laevitas.ch

Bitcoin options open interest put-to-call ratio. Source: Laevitas.ch

The indicator reached a 0.47 bottom on Aug. 29, reflecting the 50,000 BTC protective puts stacked against the 104k BTC call (buy) options. Still, the gap has been decreasing as the use of neutral-to-bearish put contracts started to get traction after the Sept. 24 monthly expiry.

According to Bitcoin futures and options markets, it might seem premature to call a ‘bearish’ period, but the last two weeks show absolutely no signs of bullishness from derivatives indicators. It appears that bulls’ hope clings on to the ETF deadline acting as a trigger to break the current market structure.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.