Since 2013 the Grayscale Bitcoin Trust Fund (GBTC) has offered its investors exposure to Bitcoin (BTC) through a publicly quoted private instrument. However, the trust’s convertibility and liquidity vastly differ from an Exchange Traded Fund (ETF).

Trusts are structured as companies, at least in regulatory form, and are ‘closed-end funds’ which can initially only be sold to accredited investors. This means the number of available shares is limited, and retail traders can only access them via secondary markets. Furthermore, a GBTC share cannot be redeemed for the underlying BTC position.

Historically, GBTC used to trade above the equivalent BTC held by the fund, which was caused by the retail crowd’s excess demand. The common practice for institutional clients was to buy shares directly from Grayscale at par and sell at a profit after the six-month lock-up period.

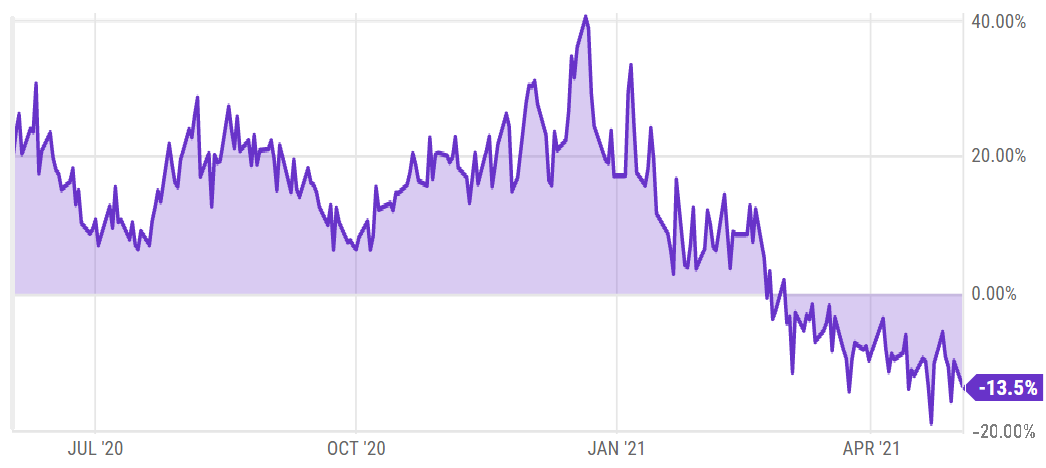

During most of 2020, GBTC shares traded at a premium to its Net Asset Value (NAV), which varied from 5% to 40%. However, this situation drastically changed in March 2021. The approval of two Bitcoin ETFs in Canada heavily contributed to extinguishing the GBTC premium.

ETF funds are less risky and cheaper compared to trusts. Moreover, there is no lock-up period, and retail investors can attain direct access to buy shares at par. Therefore, the emergence of a better Bitcoin investment vehicle seized much of allure that GBTC once possessed.

Can DCG save GBTC?

Grayscale GBTC premium vs. net assets value. Source: Ycharts

Grayscale GBTC premium vs. net assets value. Source: Ycharts

In late February, the GBTC premium entered adverse terrain, and holders began desperately flipping their positions to avoid getting stuck in an expensive and non-redeemable instrument. The situation deteriorated up to an 18% discount despite BTC price reaching an all-time high in mid-March.

On March 10, Digital Currency Group (DCG), Grayscale Investments’ parent company, announced a plan to purchase up to $250 million of the outstanding GBTC shares. Although the conglomerate did not specify the reason behind the move, the excessive discount certainly would have pressured their reputation.

As the situation deteriorated, DCG announced a roadmap for turning its trust funds into a U.S. ETF, although no specific guarantees or deadlines have been informed.

On May 3, the firm announced that it had purchased $193.5 million worth of GBTC shares by April. Moreover, DCG increased its GBTC shares repurchase potential to $750 million.

Considering the $36.3 billion in assets under management for the GBTC trust, there’s reason to believe that buying $500 million worth of shares might not be enough to ease the price discount.

Because of this, some important questions arise. For example, can DCG lose money by making such a trade? Who’s desperately selling, and is a conversion to an ETF being analyzed?

Looking forward

As the controller of the fund administrator, DCG can buy the trust fund’s shares at market prices and withdraw the equivalent Bitcoin for redemption. Therefore, buying GBTC at a discount and selling the BTC at market prices will consistently produce a profit and there’s no risk by doing this.

Apart from a few funds that regularly report their holdings, there’s no way to know who has been selling GBTC below net asset value. The only investors with 5% or more holdings are BlockFi and Three Arrows Capital, but none have reported reducing their position.

Therefore, it could be potentially multiple retail sellers exiting the product at any cost, but it is impossible to know right now.

While buying GBTC at a 10% or larger discount might seem a bargain at first, investors must remember that as of now, there’s no way of getting out of those shares apart from selling it at the market.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.