In any market, whether it is fruit and vegetables or financial assets, prices are determined by the intersection of supply and demand.

If tomatoes are scarce due to a flood, with the same demand, the price in the supermarket will inevitably be higher — just as it will be higher if, with the same supply, twice as many people want to buy tomatoes.

In the financial market, if supply is unlimited, the price is not changed by demand, as in the case, for example, of a mutual fund.

Related: Don’t be naive — BlackRock’s ETF won’t be bullish for Bitcoin

If more subscribers want to buy this fund, more shares are simply issued at something called net asset value (NAV) — that is, the correct value of the fund’s assets.

For example, let’s suppose a fund has a capitalization of $100 million, made up of 10 million units at a value of $10. If an investor wants to invest $10 million, 1 million units are issued at a value of $10, and the capitalization of the fund becomes $110 million.

It would be a different story if the shares available were limited to 10 million, so anyone who wanted to buy the shares would have to find someone willing to sell them. In that case, the price might no longer be $10, but it would depend on how much the buyer was willing to pay and how much the seller wanted to earn. It would create a situation in which the price fluctuated according to uneven supply and demand. If an asset was in high demand, obviously, the price could go much higher than the correct price.

But how can you estimate the correct price?

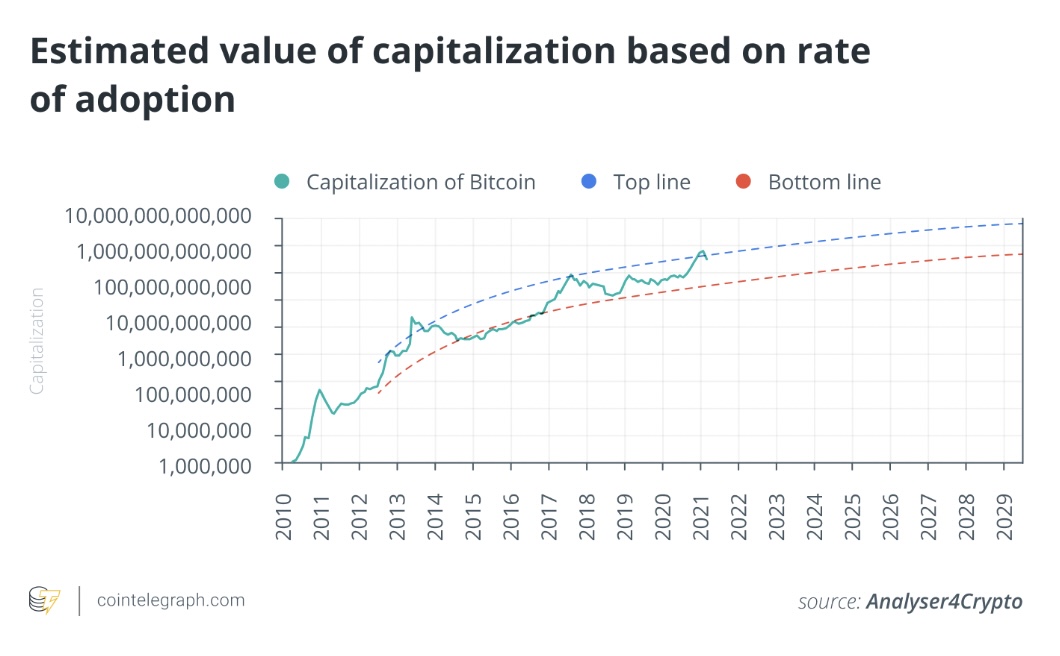

In 2021, I published data that attempted to estimate the fair value price of Bitcoin, illustrated in the graph below. It suggested that in June of that year, we had reached a relative maximum for Bitcoin (BTC). (I hoped at the time it would not prove true, but it did.) How had I estimated this value?

The previous fund example helps us understand the logic behind this estimation.

If the capitalization of a fund is given by the number of units outstanding multiplied by the NAV, or the price, it is also true that it could also be estimated as the number of investors in the fund per average amount held by each investor.

So, in the case of Bitcoin, if I would be able to estimate the average amount held in each wallet by

the number of wallets in circulation, I can also estimate the capitalization of the Bitcoin and, consequently, by dividing by the number of Bitcoin in circulation, derive its price.

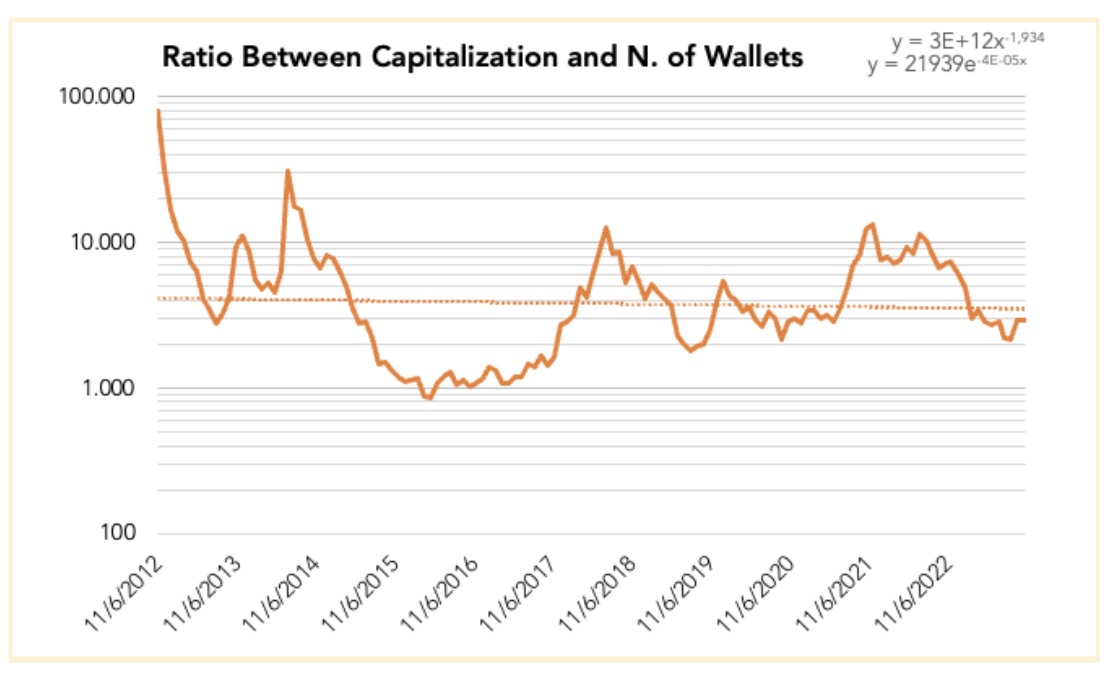

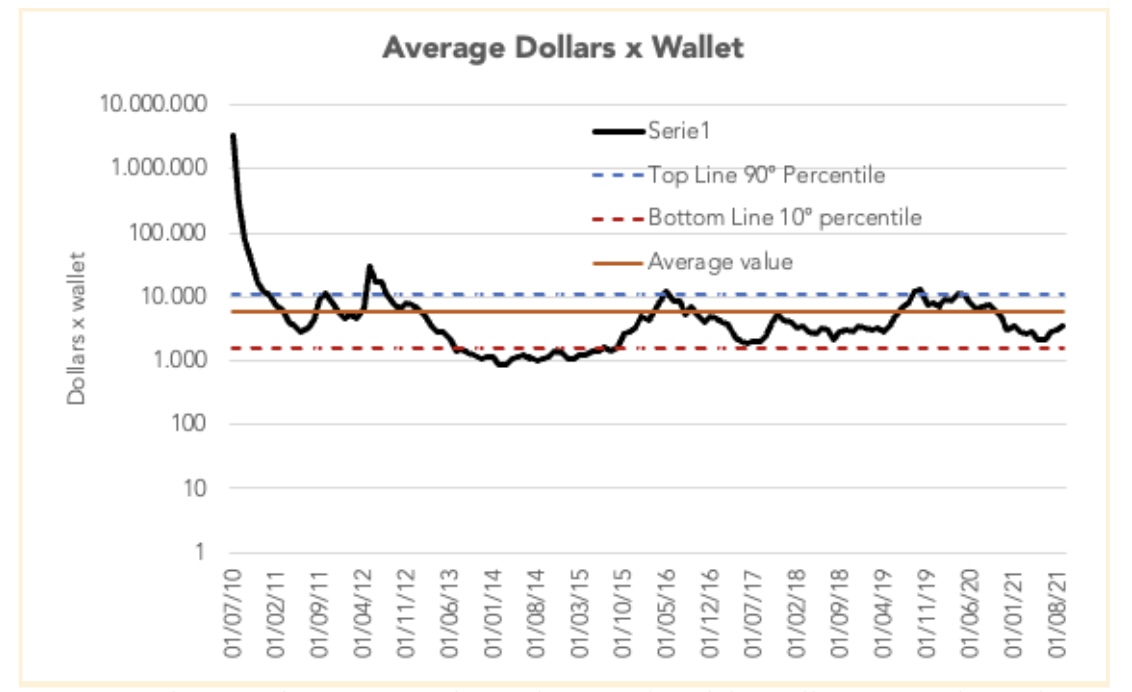

Luckily for us, the transparency offered by the blockchain allows us to collect much of this information with a high degree of reliability. For example, the number of Bitcoin addresses with a balance different than zero can be easily tracked just by running a network node.

As can be seen from the graph, the average amount (United States dollars) in wallets fluctuates due to supply and demand (many wallets hold Bitcoin without ever moving it), so if we take the 90th percentile and the 10th percentile, we can find a range that can lead us to subsequently estimate the price of Bitcoin.

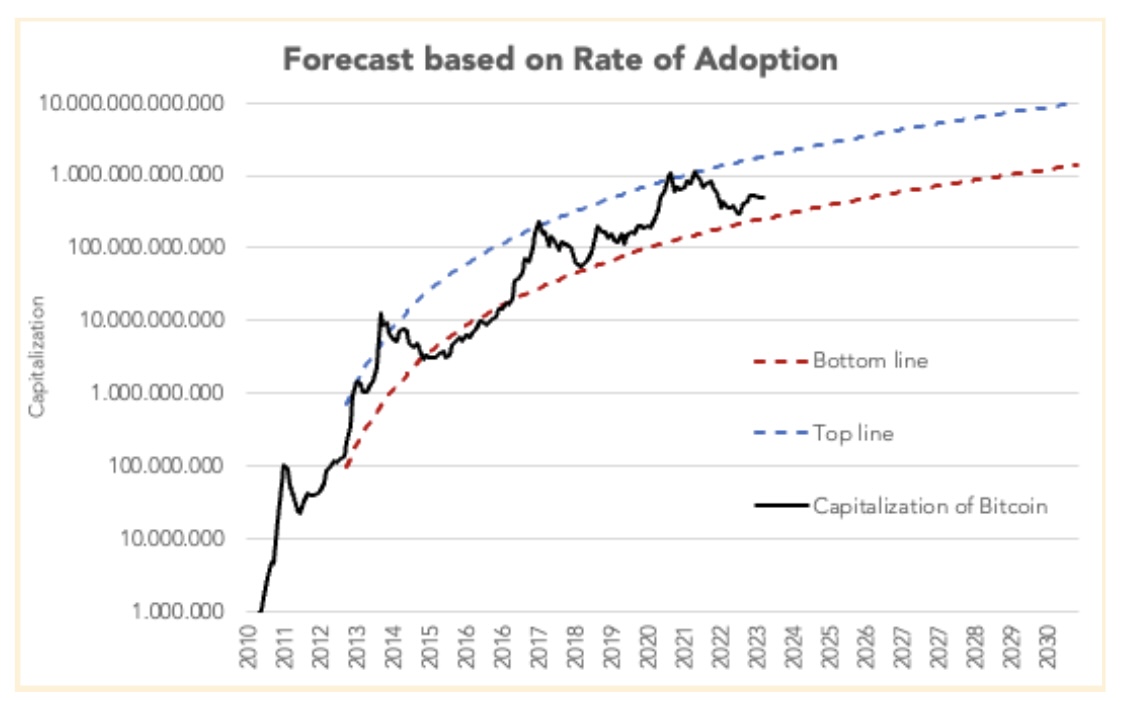

Now, once the growth curve (on a logarithmic scale) of the wallets in circulation has been estimated, it is possible to estimate a range within which the price of Bitcoin should move.

This model is simple, but the simplicity is its strength: we do not know if a user owns different addresses or if a single address is “owned” by multiple users — as in the case of the cold wallet of an exchange — but we can rely on these relationships especially when compared in terms of large numbers and on a time horizon of a complete price cycle.

Related: Bitcoin ETFs: Even worse for crypto than central exchanges

For example, in the last days of a crypto winter — like in recent months — typically, we can detect an increase in withdrawals from crypto exchanges and a reduction in balances held in these centralized platforms. Since keeping crypto assets in third-party custody is usually considered more dangerous, this signal is considered bullish since it shows the preference for investors to hold a long Bitcoin position in the long term rather than holding it in a trading account to take advantage of short-term speculative opportunities.

This phenomenon is therefore accompanied by an increase of addresses (withdrawal from a few cumulative cold wallets to fill many single addresses controlled by individual persons) and lays the foundations for a cyclical price appreciation also based on the model described in this article.

Data from this graph and this model indicate the price of Bitcoin could reach its next ceiling in autumn 2025 at $130,000 — and possibly higher.

As always, it is important to note that this forecast is not financial advice. It can only be taken as an expected value based on some assumption with a certain degree of confidence. But similar price growth estimates also emerge from other predictive models. The recent surge of interest in this asset class among institutional players like BlackRock — the largest asset manager in the world, which is seeking approval for a spot Bitcoin exchange-traded fund — may indicate that they place some faith in these models.

Daniele Bernardi is the founder of Diaman, a group dedicated to the development of profitable investment strategies. He is also the chairman of Investors’ Magazine Italia SRL and Diaman Tech SRL, and is the CEO of asset management firm Diaman Partners. In addition, he is the manager of a crypto hedge fund. He is the author of The Genesis of Crypto Assets, a book about crypto assets. He was recognized as an “inventor” by the European Patent Office for his European and Russian patents related to the mobile payments field.

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.