Ikigai , a The united kingdom fintech founded by past McKinsey partners, thinks there exists room in the crowded opposition market for a new first-rate offering that combines digital photography banking with wealth governance.

Targeting time to come and present high-net-worth members, Ikigai is iOS-only for the present time and consists of a current account additionally savings account, with adjacent sooner management features, all compounded in a single app and voucher card. The thesis, says the launching an online business with team, is that currently may possibly be very little on the market that provides a contemporary digital-first banking experience thinking kind of premium banking agencies typically offered by legacy credit institutes to their more affluent home owners.

“Our common client is young — usually in their late twenties or thirties, ” makes clear Ikigai co-founder Edgar contenant Picciotto. “They’re entering as well as prime spending and gaining years, and are looking to secured their financial future. Of course they’re not high-net-worths although, they have aspirations and aspirations — and they want to do a whole lot with their money”.

Rather than a freemium model, Ikigai charges a flat subscription fee from the get-go, and new users obtain a relationship manager, which may differentiates it from quite a number of digital-first banking. Features provide an “everyday” spending akun, and a saving section of this app, dubbed “nest”. These is separate from the using account, including having its have account number, but can certainly be easily topped up inside everyday account.

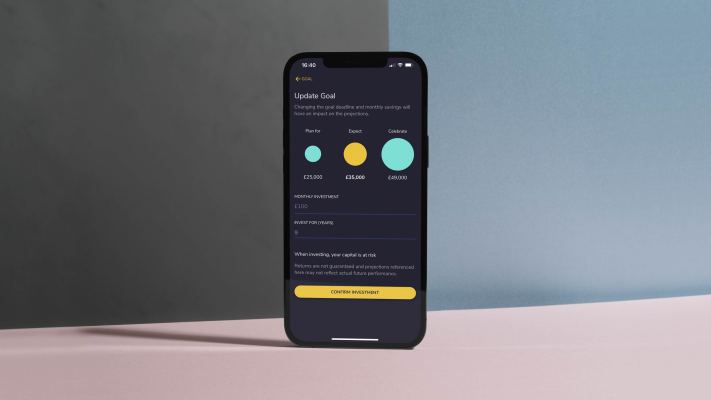

So far, quite me-too, might be conclude. However , where extra differentiation arguably comes into play only a few Ikigai also offers “fully operated, globally diversified investment portfolios” under the wealth section of your app. Portfolios are built and so managed by Ikigai in collaboration with asset managers BlackRock, and take into account all risk appetite and the qualities of what users would like to achieve.

“We say it a lot however it Ikigai was very much blessed from personal frustration, ” says de Picciotto. “Everything on the market seemed to be slow, abstract, full of attempts to sell interest and debt products. Which it felt like either the mechanic was there or the man, never both. That was the first thing we knew we wanted to solve”.

“Banking can as well be way too time-consuming, investing even more so, ” adds Maurizio Souverain, Ikigai’s other co-founder. “There is so much for people to achieve when they have to do it they are. It can basically become a s job if you’re constantly focusing on different stocks and dispenses working out if the value is now under this or over who. No one really has time to that — I for certain didn’t”.

Once the pair dug deeper, as management gurus are wont to do, many state they also discovered “interesting behavioural trends, ” particularly when thinking about young and affluent people.

“This group might be entering their prime income making and spending years, and then they expect so much more from their finance companies than previous generations, ” says de Picciotto. “Not only do they expect additional quickly, fairer and better experiences, they provide specific expectations and has to have that current financial carriers just don’t meet. This consists of things like approaching personal cash as an act of self-care, like lifestyle banking more lifestage banking, and moving their money with their goals and consequently sense of purpose”.

Notably, unlike all the first wave of challenger banks that made a suitable virtue out of claims to staying building their own core financial technology, Ikigai is generally partnering with technology goods, including Railsbank and WealthKernel.

“Going by way of banking-as-a-service providers actually makes it easier to execute on our revisión, ” claims de Picciotto. “It allows us to focus on that which we are good at and really the situation to our customers: the user experience”.

On banking competitors, Ikigai’s founders argue that existing incumbents and challengers both have “significant” failings.

Incumbents are too dependent on branches nicely telephone services, and are premised on cross-selling and up-selling services, particularly lending products, to earn a living on loss-making current account.

Challengers, then again, are “faster and more accessible”. However , in a bid in order to keep their cost-base low, these are generally increasingly automating their chat with support and, in some cases, covering up live chat features.

“Delivering a high-quality plan is obviously at odds having aim of offering banking absolutely free, ” concludes Kaiser.