The May 19 crypto market sell-off saw $1.2 trillion in value erased from the total market capitalization as the froth and excess leverage of over-hyped markets was quickly eliminated.

But similar to a forest fire, whose destructive power is essential to the rejuvenation of a forest’s ecosystem, dramatic market shake-outs are a vital part of the full life cycle of a developing market, as excesses that have accumulated are burned away and cleared in order to set the stage for a new round of growth.

According to data from Glassnode, the past month saw a “historically large decline” in on-chain activity, “transitioning rapidly from booming on-chain economies at ATH prices, to almost completely clear mempools and waning demand for transactions and settlement.”

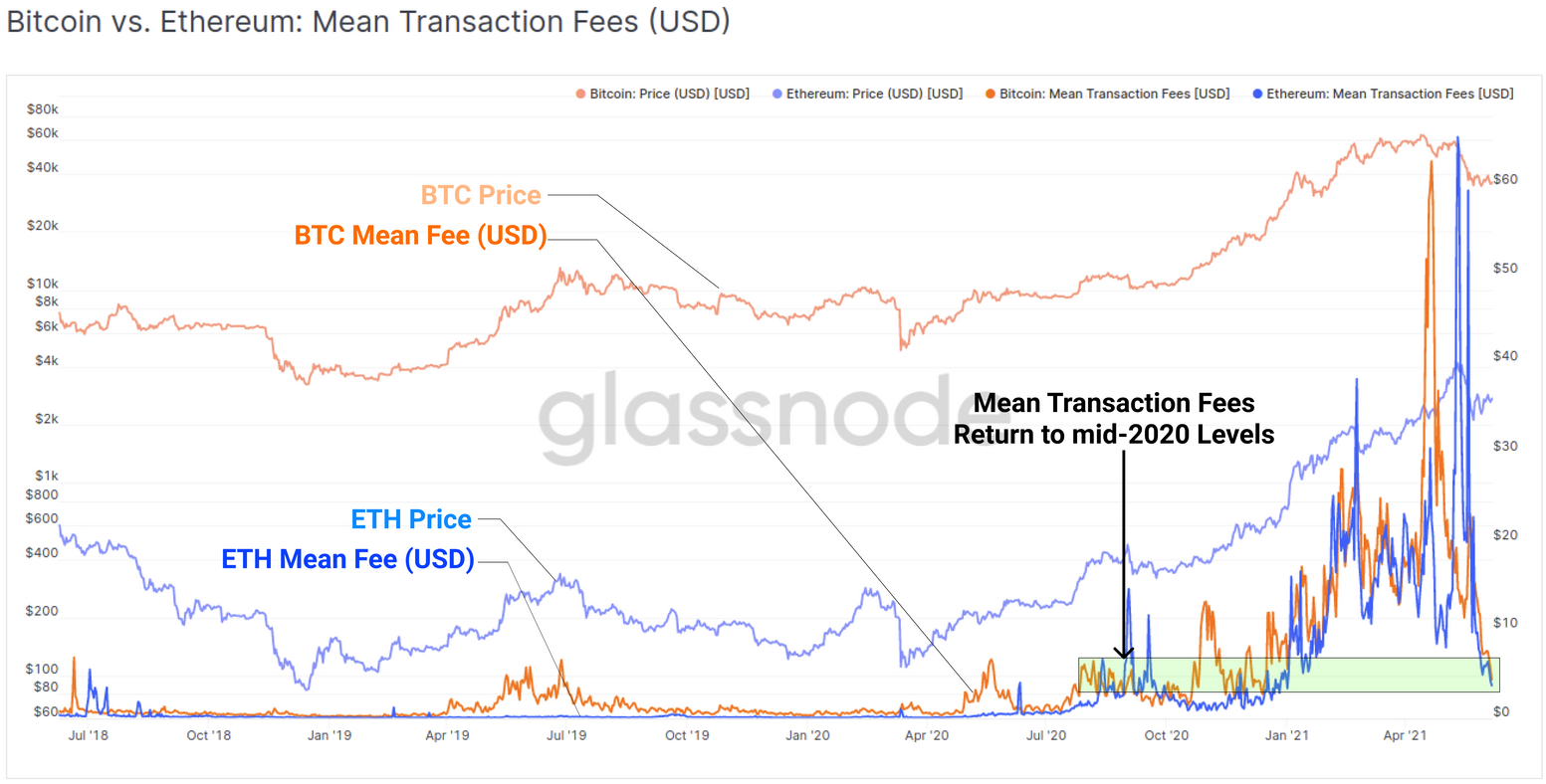

This clearing of congestion helped address the rising cost of fees on both the Ethereum (ETH) and Bitcoin (BTC) networks which have now “returned to mid-2020 levels of around $3.50 to $4.50” after experiencing short term spikes as high as $60 in April and May but given the lingering price action from BTC and Ether, traders are also worried whether the market has shifted from bullish to bearish.

Bitcoin vs. Ether average transaction fee. Source: Glassnode

Bitcoin vs. Ether average transaction fee. Source: Glassnode

The drop in activity has resulted in a 65% decline in the total USD denominated transfer volume settled by the Bitcoin network and a 60% decrease in value transferred on Ethereum, marking the second largest declines for the networks behind the 80% drop for Bitcoin in 2017 and the 95% drop for Ethereum in 2018.

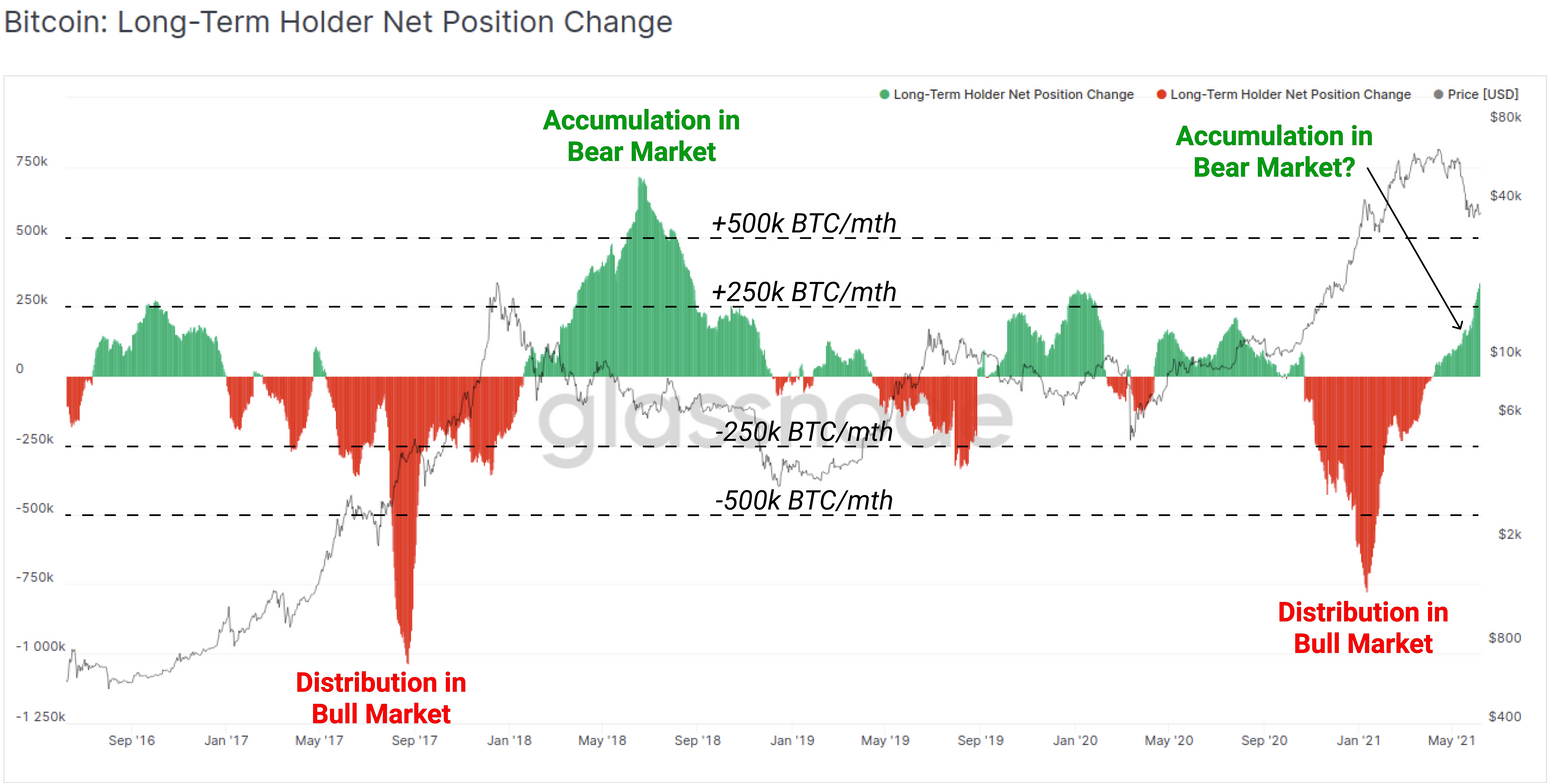

Long term holders accumulate

Although the on-chain activity paints a grim picture for some, as short-term holders were the hardest hit by the downturn, a closer look shows that long-term holders (LTH) have started accumulating again, a sign that the worst of the shake-out may have passed.

Long-term holder net position change. Source: Glassnode

Long-term holder net position change. Source: Glassnode

As seen in the chart above, the supply held by long-term BTC holders has begun to accelerate upward following a period of distribution that happened as the price rallied from $10,000 to $64,000. This rising figure indicates that the “LTH supply is now in a firm uptrend,” and is similar to the trend seen during the “late 2017 bull and early 2018 bear.”

Glassnode said:

“This fractal describes the inflection point where LTHs stop spending, start re-accumulating and hodling what are now considered cheap coins.”

Further bullishness can be found in the fact that the amount of BTC currently held by LTHs is 2.3 million more than at the peak of 2017, indicating that the long-term view of these token holders is that the market is headed higher.

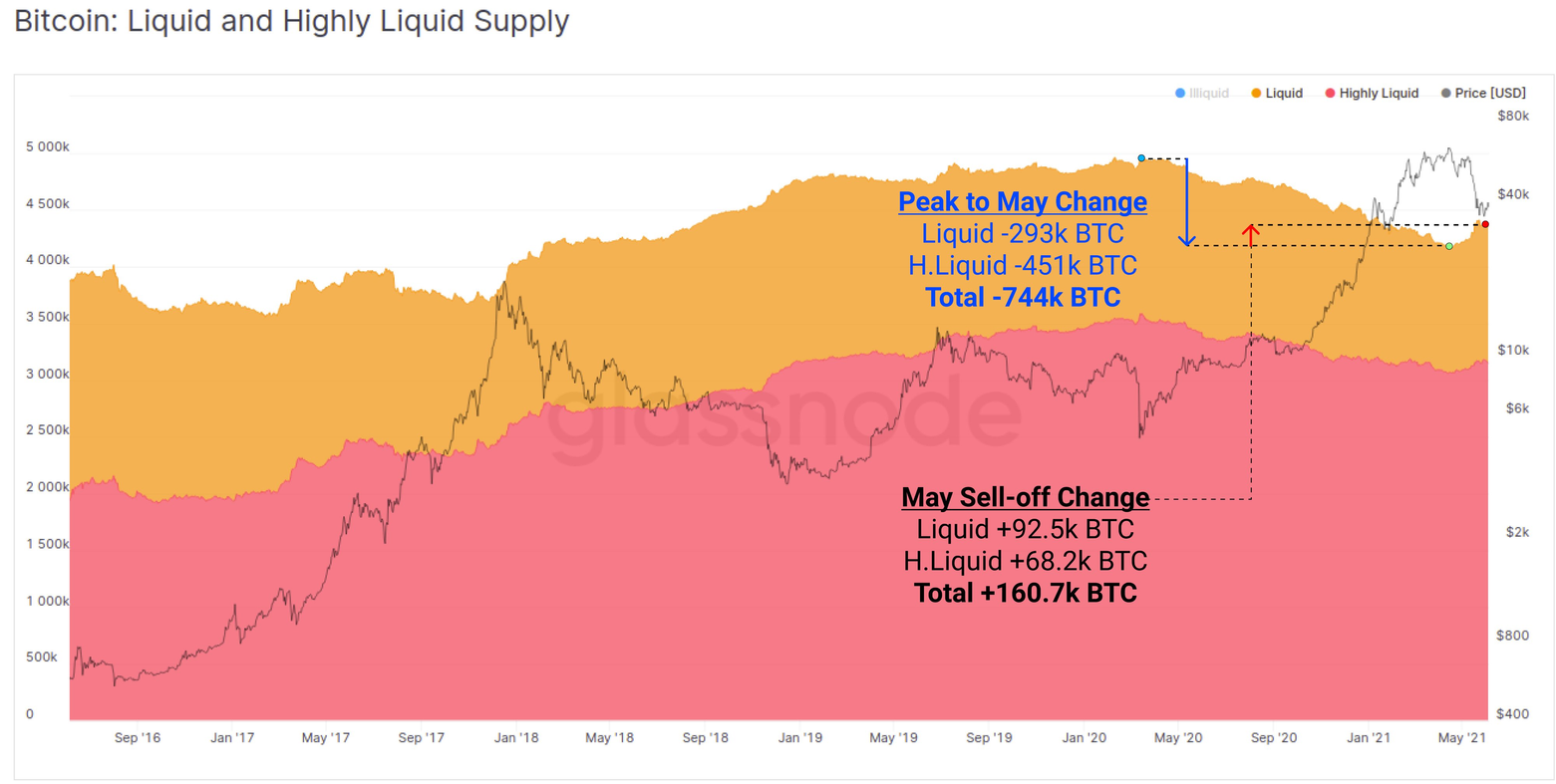

One final indication that the market may be consolidating in preparation for its next move higher can be found looking at the change in the liquid and illiquid supply of BTC over the past 6 months.

Bitcoin liquid and highly liquid supply. Source: Glassnode

Bitcoin liquid and highly liquid supply. Source: Glassnode

As seen in the chart above, 160,700 BTC went from an illiquid state back into liquid circulation during the month of May, representing just 22% of the total supply that moved from liquid to illiquid since March 2020.

This means that 78% of the BTC acquired since then remains unspent, indicating an overall positive outlook by long-term holders.

While it’s impossible to be certain about the next steps for the cryptocurrency market thanks to factors like unpredictable volatility, erratic tweets from influencers and the rumors of surprise government crackdowns, on-chain data indicates a positive long-term outlook that should resume once the current shake-out and consolidation periods subside.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk, and you should conduct your own research when making a decision.