Tax management is an essential component that can have a big impact on your overall savings and investment results. The implementation of efficient tax planning tactics is crucial, regardless of whether you are involved in conventional financial markets or are looking at prospects in the cryptocurrency field.

This article will discuss important factors for maximizing tax savings in both the traditional financial markets and the cryptocurrency space.

Understand tax laws and regulations

Understanding the tax laws and regulations that apply to your investments is the first step in efficient tax planning. This includes comprehending capital gains taxes, dividend taxes and any related tax credits or deductions in traditional financial markets.

Regulations in the cryptocurrency industry are evolving, and local tax laws may differ. Learn about the tax repercussions of investing in cryptocurrencies, including the definition of cryptocurrencies as assets, the need for tax reporting and any applicable exemptions.

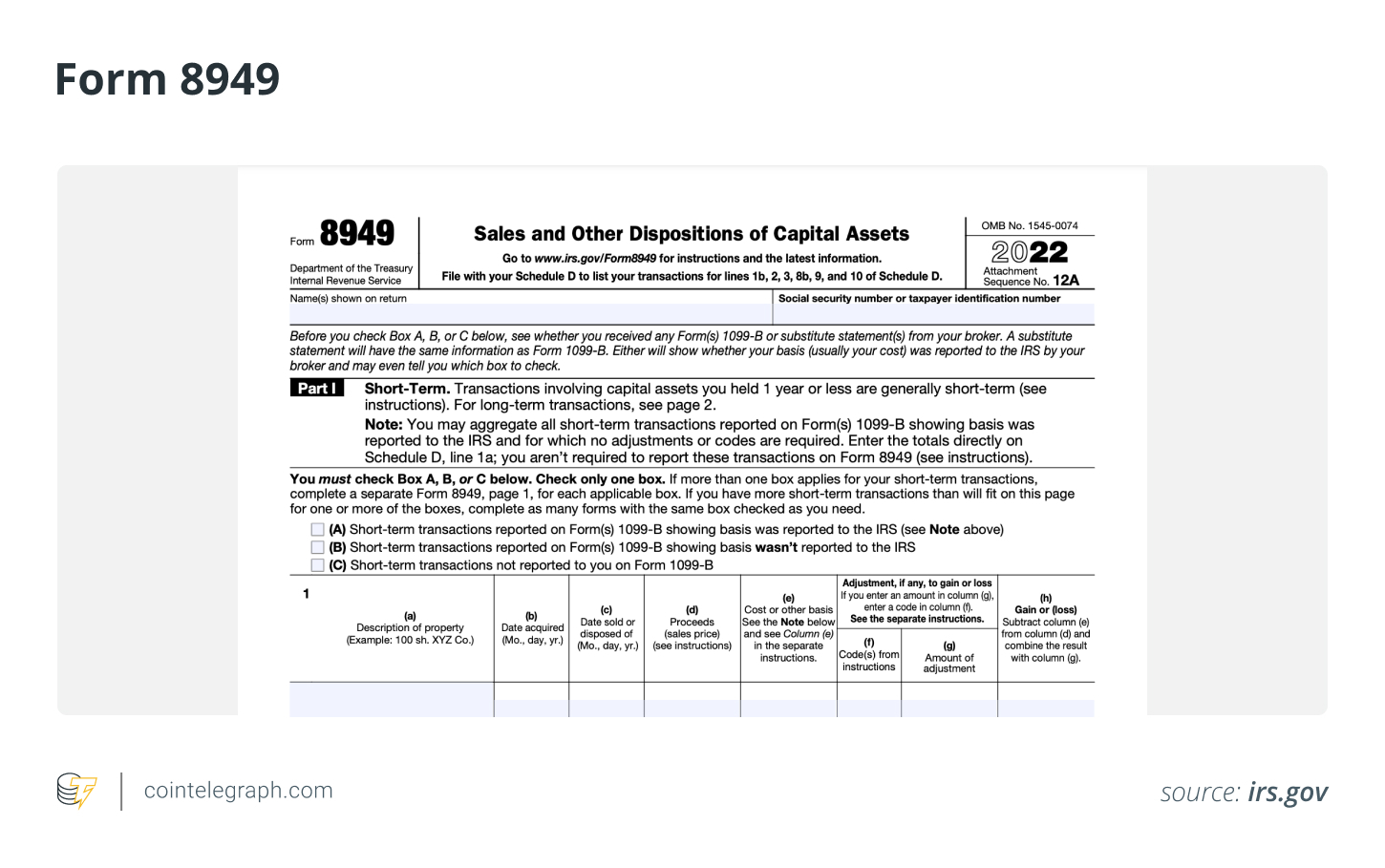

For instance, when it comes to accurately documenting transactions involving assets that may result in capital gains or losses, Form 8949 is your go-to resource. This versatile form encompasses a wide range of assets, including digital assets, stocks, bonds and more. By diligently utilizing Form 8949, you can ensure thorough and accurate reporting of your financial activities while complying with tax regulations.

Related: A beginner’s guide to filing cryptocurrency taxes in the US, UK and Germany

Select tax-advantaged accounts

One effective strategy is to leverage tax-advantaged accounts available in traditional financial markets, such as individual retirement accounts (IRAs) or 401(k) plans. Contributions to these accounts may offer immediate tax advantages, such as tax-deferred growth or tax-free withdrawals during retirement.

Investigate cryptocurrency opportunities, such as self-directed IRAs, which allow cryptocurrency investment within the framework of a tax-advantaged account, potentially postponing taxes on cryptocurrency earnings.

Harvest tax losses

To balance capital gains and lower taxable income, selling investments that have incurred losses is known as “tax-loss harvesting.” Review your portfolio carefully and think about selling underperforming assets in the traditional financial markets in order to realize losses that can counteract gains.

By selling cryptocurrencies that have lost value, tax-loss harvesting can likewise be used in the cryptocurrency world. However, keep in mind that the wash-sale rule forbids repurchasing the same or nearly similar assets within a predetermined time frame.

Related: What are wash trading and money laundering in NFTs?

Utilize holding periods

Keeping investments for a specific amount of time can have a big tax impact. Long-term capital gains are typically taxed at lower rates than short-term gains in conventional financial markets. For long-term capital gains tax treatment, think about holding investments for more than a year.

Similar to this, owning cryptocurrencies for more than a year may result in tax benefits in the crypto space. However, tax laws governing cryptocurrencies may vary, so speaking with a tax expert may help you comply.

Seek professional guidance

Due to the complexity of tax planning in both conventional and cryptocurrency financial markets, seeking professional advice may help you stay compliant with the laws applicable in your jurisdiction.

A tax expert with knowledge of investments and cryptocurrencies can offer insightful advice, guide you through ever-changing legislation, and help you develop tailored tax planning methods that maximize your savings. Additionally, they can guarantee correct reporting and adherence to tax rules.

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.