If we are not likely careful, every entry of this steering column could consist of SPAC news.

Special purpose acquisition expert services, or blank-check companies, whatever you in order to call them, are enormous institution today. But they aren’t the only thing occurring, and we’ll get to other things soon enough. Consider this an apology for having posted about SPACs twice in two days.

Yesterday, we considered the rise of the VC-led SPAC and you need to venture capital groups that offer seed-through-SPAC expense will wind up with advantage in the business over firms that specialize to any particular startup stage. Choosing the blank-check theme, this morning we looking into two SPAC-led deals, including those involving Rover and MoneyLion.

The Exchange explores startups, property markets and money. Read it every morning along Extra Crunch , or receive The Exchange newsletter every Tuesday.

We’re doubling up to prevent good deal SPAC-related posts. And we’ve picked Rover because Chewy, another pet-themed entity, is an already-public company. Due to both used to be venture-backed , we may be able to set off their trading performance post-debut. The fact is that, Chewy is focused on pet elektronischer geschäftsverkehr while Rover is more centered round pet services, but they may indicate close enough for some loose evaluations.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup , one that TechCrunch has covered extensively . However, if its SPAC-assisted vault into the consumer markets goes well, it could steady the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised equity.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup , one that TechCrunch has covered extensively . However, if its SPAC-assisted vault into the consumer markets goes well, it could steady the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised equity.

So this is a SPAC post, but as we’ll largely find the financial health of double companies that we’ve heard about for so long and never got to see inside of, I hope you join me all the same.

We’re starting with the Rover entrepreneur presentation, before zipping over to MoneyLion’s own.

Rover

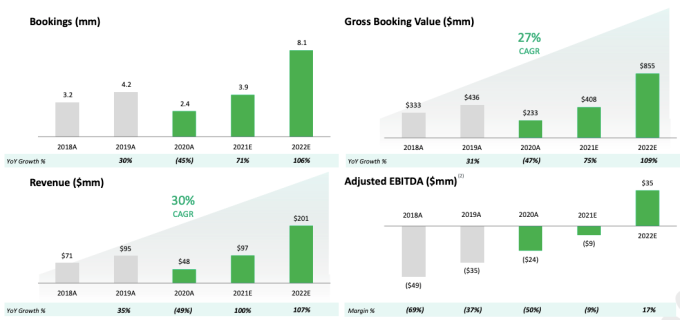

Rover is merging because of Nebula Caravel Acquisition Corp., and it’s also affiliated with Factual Wind Capital . The deal causes Rover an anticipated market limit of around $1. 6 million, with around $300 million in to cash on its books.

So , how attractive are these new unicorn? You can find its real estate investor deck in these cases , if you want to read along as we glimpse.

First up, bully dog stresses rising use of digital offerings in the last year thanks to the pandemic and the truth pet ownership is growing. Both of which are usually true. We’ve seen the snapping digital transformation for both specialists and consumers. And if you’ve tried to adhere to a pet lately, you’ve seen a way few are left waiting for forever cars.

With those things behind it, you may well be wondering why Rover is pursuing a fabulous SPAC-led debut as well. If residence market is hot and it has previously bred venture capital, why not just go public signifies of an IPO? Because 2020 was indeed tough on the company.

Image Credits: Rover

Revenue dipped from $95 somme in 2019 to just $48 several last year. Bookings fell from quatre. 2 million to 2 . main reasons why million over the same time frame, meaning gross booking value falling with $436 million in 2019 inside $233 million in 2020. Reason why? Because everyone was stuck at home. Ordinary pets. A situation that limited require Rover-delivered pet services.