Bitcoin (BTC) has breached the $50,000 level on Feb. 16. But while failing to cleanly break the psychological barrier, it undoubtedly displayed the potential for even higher valuations.

Meanwhile, futures and options indicators are misaligned, signaling excessive buyers’ leverage, while options markets remain calm. After analyzing both markets, one might theorize what has caused this apparent incongruence.

Options skew remained neutral-to-positive

When analyzing options, the 25% delta skew is the single-most relevant gauge. This indicator compares similar call (buy) and put (sell) options side-by-side.

It will turn negative when the put options premium is higher than similar-risk call options. A negative skew translates to a higher cost of downside protection, indicating bullishness.

The opposite holds when market makers are bearish, causing the 25% delta skew indicator to gain positive ground.

Deribit 30-day BTC options 25% delta skew. Source: laevitas.ch

Deribit 30-day BTC options 25% delta skew. Source: laevitas.ch

A skew indicator between negative 10% (slightly bullish) and positive 10% (somewhat bearish) is considered normal. Over the past three months, there hasn’t been a single occurrence of a 10% or higher 30-day skew, which is usually considered a bearish event.

This data is very encouraging, considering that Bitcoin saw a 24% correction on Jan. 11, in addition to a 19% sell-off ten days later. Yet, there is no evidence that options traders demanded more significant premiums for downside protection.

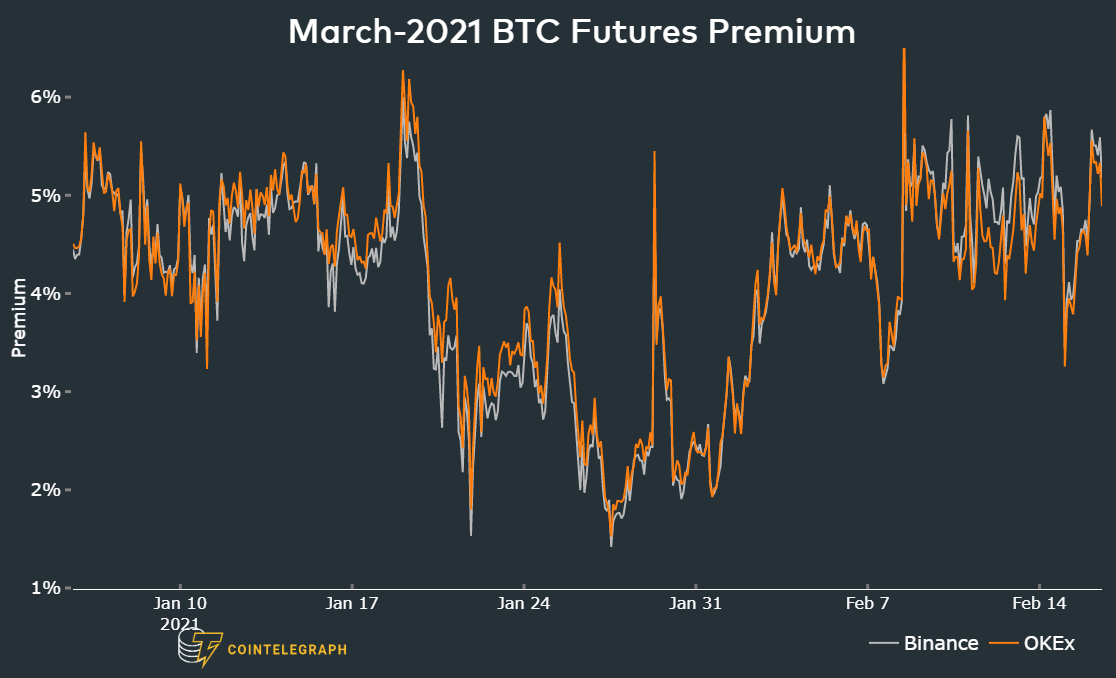

Futures premium held excessive-optimistic levels

By measuring the expense gap between futures and the regular spot market, a trader can gauge the level of bullishness in the market.

The 3-month futures should usually trade with a 6% to 20% annualized premium (basis) versus regular spot exchanges. Whenever this indicator fades or turns negative, this is an alarming red flag. This situation is known as backwardation and indicates that the market is turning bearish.

On the other hand, a sustainable basis above 20% signals excessive leverage from buyers, creating the potential for massive liquidations and eventual market crashes.

Mar. 2021 BTC futures premium. Source: NYDIG Digital Assets Data

Mar. 2021 BTC futures premium. Source: NYDIG Digital Assets Data

The above chart shows that the indicator bottomed at 1.5% on Jan. 27 but later reverted to 4.5% and higher as Bitcoin rebounded above $35,000. Even during its darkest periods, the futures premium held above 10% annualized rate, indicating optimism from professional traders.

Meanwhile, the current 5.5% level, equivalent to a 50% annualized rate, indicates excessive buyers’ leverage. Perpetual futures (inverse swaps) could be the root of this issue, and retail traders more widely use those contracts.

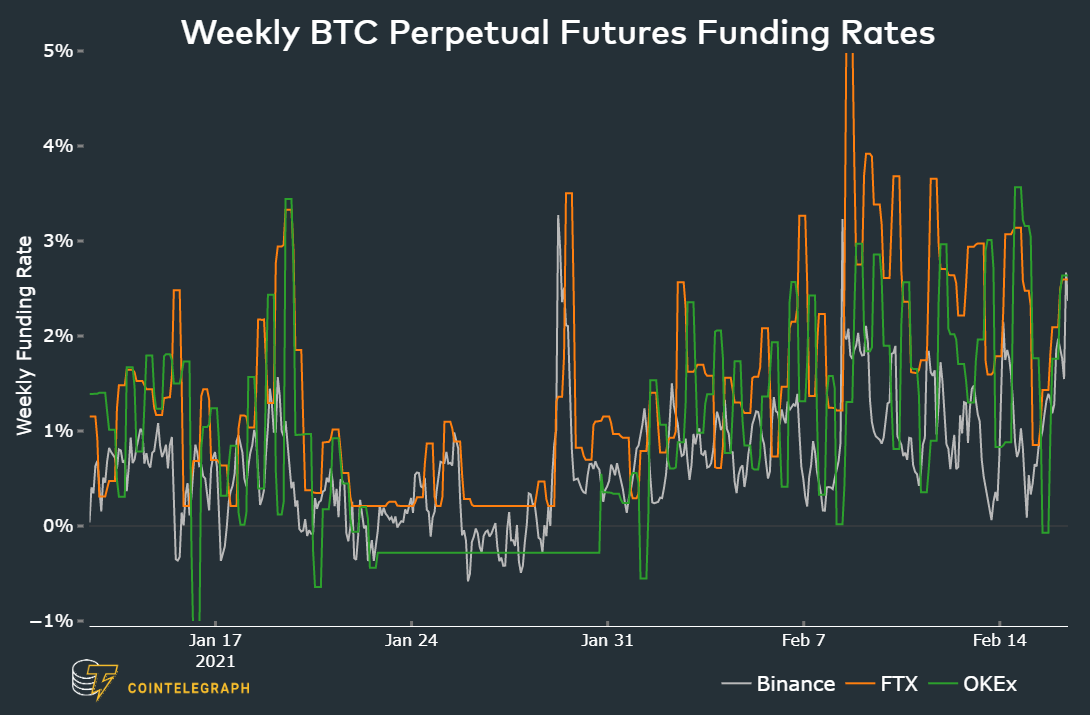

Weekly BTC perpetual futures funding rate. Source: NYDIG Digital Assets Data

Weekly BTC perpetual futures funding rate. Source: NYDIG Digital Assets Data

Take notice as the funding rate has exceeded 2.5% per week, thus more than compensating the 50% annualized premium of the March contracts.

Therefore, arbitrage desks and market makers are likely happy to pay such a hefty premium on fixed-month contracts while simultaneously shorting the perpetual future and profit from the rate difference.

To conclude, this movement perfectly explains why options markets are relatively neutral while futures markets show excessive buyers’ leverage. While institutional clients and whales dominate options volumes, retail traders seem to be the root of such mismatch.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.