2022 has been a bumpy year for the cryptocurrency market, with one of the worst bear markets on record and the downfall of some major platforms within the space. The global economy is beginning to feel the consequences of the pandemic, and clearly, this has had an influence on the crypto industry.

Below is a breakdown of some of the biggest disappointments in the crypto space this year.

Axie Infinity’s Ronin Bridge hacked

In March of this year, Ronin, the blockchain network that runs the popular nonfungible token (NFT) crypto game Axie Infinity, was hacked for $625 million. The hacker took 173,600 Ether (ETH) and 25.5 million USD Coin (USDC) from the Ronin bridge in two transactions.

When the Lazarus Group started its attack, five of the nine private keys for the Ronin Network’s cross-chain bridge were hacked. With this vote, they authorized two withdrawals totaling $25.5 million in USDC and 173,600 ETH.

According to the Ronin group, Axie Infinity’s issues began in November 2021, when its user base had expanded to an untenable size. Consequently, the corporation’s safety rules had to be relaxed to fulfill client demand. After the initial phase of fast development was completed, the firm reduced its safety procedures.

Bridge hacks have accounted for 2/3 of the $3B that has been stolen from DeFi.@AxieInfinity‘s @Ronin_Network bridge hack has been the largest to date at $600M lost. pic.twitter.com/5IAuTqShMO

— Messari (@MessariCrypto) August 30, 2022

The main difficulty was a lack of a suitably decentralized network created by game developer Sky Mavis. The hacker acquired access to the private keys of five of Sky Mavis’ Ronin Chain’s nine validator nodes, enabling them to compromise the network. When the hackers gained control of five nodes, they essentially controlled over half of the network and were free to accept or deny whatever transactions they wanted. They obtained ETH and USDC via falsifying withdrawals.

The crime occurred on March 23, but it was only noticed on March 29, when a user reported being unable to withdraw 5,000 ETH from the Ronin bridge ATM. In the aftermath of the attack, Axie Infinity developers raised $150 million to reimburse the affected users.

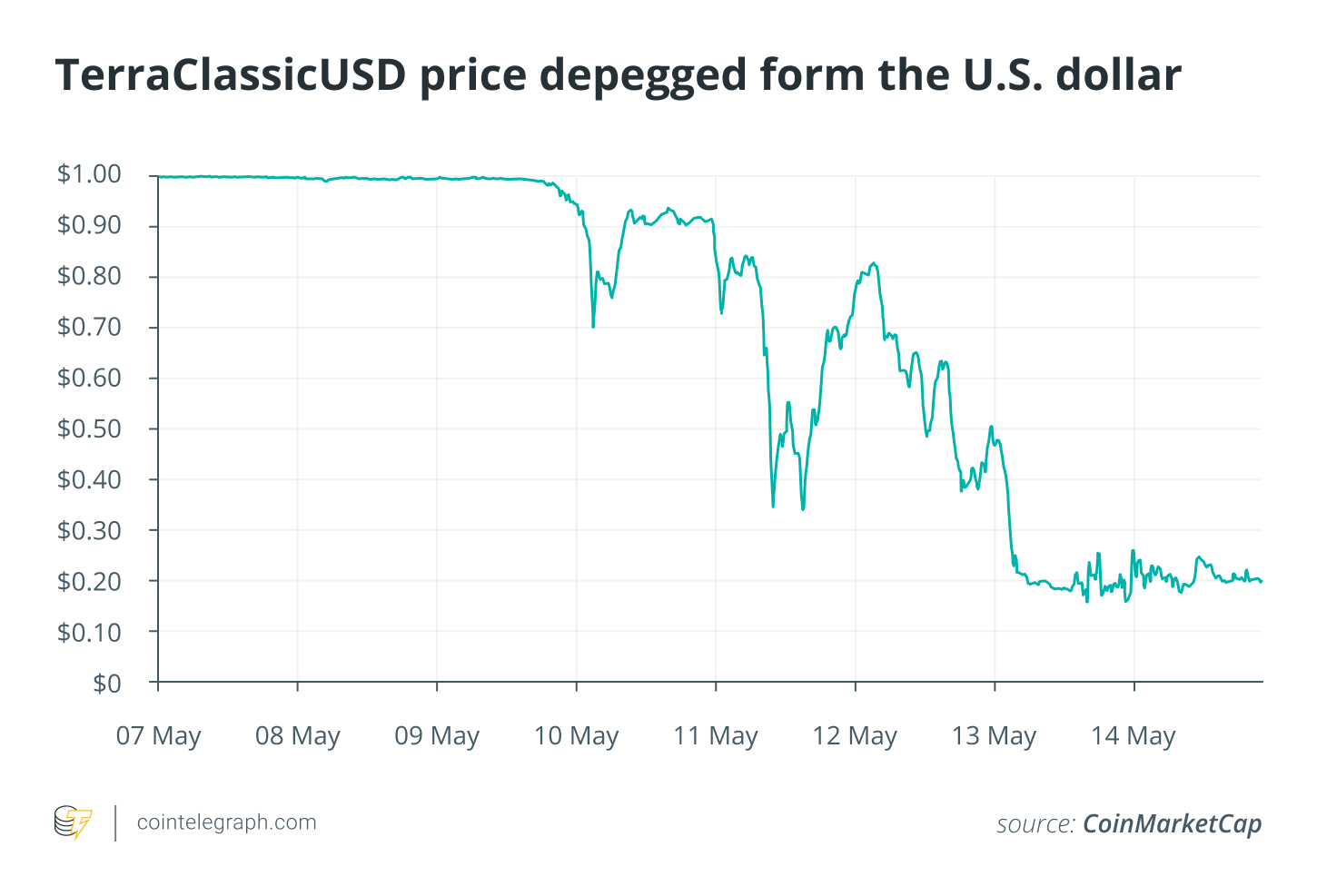

TerraUSD/LUNA collapse

On May 7, when over $2 billion in TerraUSD (UST) was unstaked (removed from the Anchor Protocol), hundreds of millions of United States dollars were quickly liquidated. It’s unclear if this was a deliberate attack on the Terra blockchain or a response to rising interest rates. Because of the enormous outflow of cash, the price of UST fell from $1 to $0.91. As a result, market players started trading $0.90 in UST for $1 in Terra (LUNA).

When a considerable amount of UST was moved out, the stablecoin depegged. The availability of LUNA increased as more people sold their UST during the panic.

Following this fall, cryptocurrency marketplaces started to suspend trading pairs such as LUNA and UST. Following the initial accident in May, Do Kwon disclosed a rehabilitation plan for LUNA, and things seemed to improve. However, the currency’s value eventually fell. It was abandoned almost as soon as it began. Finally, Terra launched a whole new currency known as LUNA 2.0.

Investors lost a combined $60 billion due to the panic selling that accompanied the decline of TerraUSD Classic (USTC) and Luna Classic (LUNC), a related token.

On Sept. 14, a South Korean court issued an arrest warrant for Do Kwon. This happened four months after Terraform Labs’ LUNA and UST tokens collapsed. Do Kwon and five others were detained for allegedly violating regional market restrictions.

Three Arrows Capital collapse

When LUNA and Terra collapsed, the crypto hedge fund Three Arrows Capital (3AC), which had a peak market valuation of more than $560 million, suffered significantly. 3AC had invested heavily in several troubled cryptocurrency projects, including the play-to-earn game Axie Infinity, which lost $625 million to a North Korean hack this year, and the centralized cryptocurrency exchange BlockFi, which laid off hundreds of employees in mid-June.

The UST collapse shattered investor confidence and expedited the slide of cryptocurrencies, which was already underway as part of a bigger flight from risk. A flood of margin calls from 3AC’s lenders sought repayment, but the firm lacked the funds to meet the requests. In addition, many of the company’s counterparties could not meet their investors’ expectations, many of whom were retail investors promised 20% annual returns.

Related: Santas and Grinches: The heroes and villains of 2022

The crypto hedge fund eventually collapsed after taking on major directional trades and borrowing from over 20 institutions, and the founders defaulted on its payments.

Because the founders would not appear in court, the lawsuit proceeded without them. In a leaked court document filed with the Singapore High Court, the Singapore government was asked to accept liquidation proceedings and work with liquidators. As liquidators try to wind down the failed crypto business of Three Arrows Capital, U.S. Bankruptcy Judge Martin Glenn has issued subpoenas to the company’s founders.

Voyager Digital’s fall

On July 6, prominent cryptocurrency investment firm Voyager Digital filed for bankruptcy after crypto hedge fund 3AC defaulted on a $650 million loan. 3AC received a significant loan from Voyager with no security. When 3AC defaulted on all of its obligations and its owners left, Voyager lost a significant sum of customer money.

Trading, withdrawals, and deposits were all suspended when Voyager reported that 3AC would not repay its loan. In June, Sam Bankman-Fried, billionaire CEO of trading firms FTX and Alameda Research, presented Voyager with a $500 million line of credit to help them weather the market collapse.

On July 5, 2022, Voyager Digital Holdings filed for bankruptcy in the Southern District of New York. According to Voyager Digital, the corporation owes between $1 billion and $10 billion to its more than 100,000 debtors. Despite its debts, however, the company believes it has assets worth between $1 and $10 billion. They also guarantee that adequate money is available to pay off the company’s unsecured creditors.

In a September court filing, insolvent cryptocurrency broker Voyager Digital revealed that it would auction off its remaining assets.

Celsius crash and liquidity crisis

Celsius’s value plummeted on July 13, 2022, when one of the main crypto businesses, Celsius Network, declared bankruptcy. As the price of cryptocurrencies fell, investors on the Celsius network started withdrawing their Bitcoin (BTC) holdings in search of safer alternatives.

Consequently, panicked investors left Celsius in volume. Despite stating they were forced to do so due to “extreme market conditions,” Celsius Network halted BTC withdrawals, swaps and transfers on June 12. Users of the site understandably thought that Celsius had declared bankruptcy and would be unable to refund their money. The value of the Celsius cryptocurrency plummeted by 70% in only a few hours and fell further in the days that followed.

The crypto market has seen a significant sell-off due to the insecurity and falling prices of many major cryptocurrencies, which corresponded with the drop in the price of Celsius. In addition, due to escalating cash flow issues, Celsius announced 23% layoffs on July 3, 2022. When the time came, the company filed for bankruptcy on July 13, 2022.

Celsius had total liabilities of $6.6 billion and assets of $3.8 billion, resulting in a $1.2 billion hole in the company’s balance sheet due to the court ruling.

FTX collapse

FTX and its U.S. equivalent, FTX.US, filed for Chapter 11 bankruptcy on Nov. 11. The exchanges collapsed due to a lack of liquidity and money mismanagement, resulting in a large number of withdrawals from fearful investors.

Following the announcement of bankruptcy, FTX.US briefly restricted withdrawals on Nov. 11, despite earlier promises that FTX.US would be unaffected by FTX’s liquidity concerns. On the evening of Nov. 11, an alleged hack took more than $600 million from FTX wallets. The assault was revealed by FTX in its assistance channel on the instant-messaging network Telegram.

PSA: If you have a bank account linked to FTX US, change your bank account password and stop sharing data immediately.

Below is a screenshot of my bank account, which they tried accessing 40 mins ago pic.twitter.com/sdnaUFEzOW

— Mike McGuiness ᵍᵐ (@mikemcg0) November 12, 2022

According to some Twitter users, hackers were also attempting to get access to FTX-linked bank accounts. Plaid, a company that connects consumer bank accounts with financial applications, responded to “concerning public reports” by denying FTX access to their products, claiming that they had no proof that their tools had been used unlawfully.

Bankman-Fried was arrested in the Bahamas on Dec. 12 at the request of the U.S. government, which wanted him extradited for eight criminal offenses, including wire fraud and conspiracy to defraud investors. Bankman-Fried was eventually deported to the United States and is awaiting trial after posting a $250 million bail.

BlockFi bankruptcy

The collapse of FTX earlier in the month generated fear and uncertainty across the market. BlockFi, another cryptocurrency exchange, filed for Chapter 11 bankruptcy on Nov. 28. With assets and liabilities ranging from $1 billion to $10 billion, the firm had over 100,000 creditors. In addition, they had a $275,000,000 debt to Sam Bankman-Fried’s American subsidiary, FTX US. The application shows that the largest client has a balance of $28 million.

Following the demise of Three Arrows Capital, multiple firms, including the crypto company that operates a trading exchange and an interest-bearing custodial service for cryptocurrencies, had serious liquidity issues.

Related: Women who made a contribution to the crypto industry in 2022

BlockFi agreed earlier this year to accept a credit package from FTX worth up to $400 million to help it weather a liquidity restriction caused by the exchange’s exposure to the TerraUSD stablecoin’s collapse. As a result of these concerns, BlockFi was reliant on the performance of the cryptocurrency exchange FTX, which may now jeopardize its financial stability.

While 2022 may have been a tough year for the crypto market, there may be a silver lining. Investor sentiment seems to be improving, and the crypto market has always recovered from previous bear markets and platform collapses. The events of 2022 could pave the way for new platforms to learn from the mistakes of their predecessors.